If you picked up the New York Times Magazine this past Sunday, you might have glanced at this week’s moral lodestone in “The Ethicist” column. It contextually condemns particular principles that a Mr. Art Babbitt held dear.

If you picked up the New York Times Magazine this past Sunday, you might have glanced at this week’s moral lodestone in “The Ethicist” column. It contextually condemns particular principles that a Mr. Art Babbitt held dear.

The printed query is in regards to suing a doctor for malpractice, even if settling out of court. The columnist, Chuck Klosterman, writes,

“There’s no ethical responsibility to bring a civil suit to trial in order to make a point.”

Babbitt took a civil suit out against Disney in December 1941 over unpaid bonuses. But today I would like to look at what may have been Babbitt’s dress rehearsal for that suit, a court case from 1935, No. 387814.

The Broadway may have looked like this, The May Department Store in LA, 1933

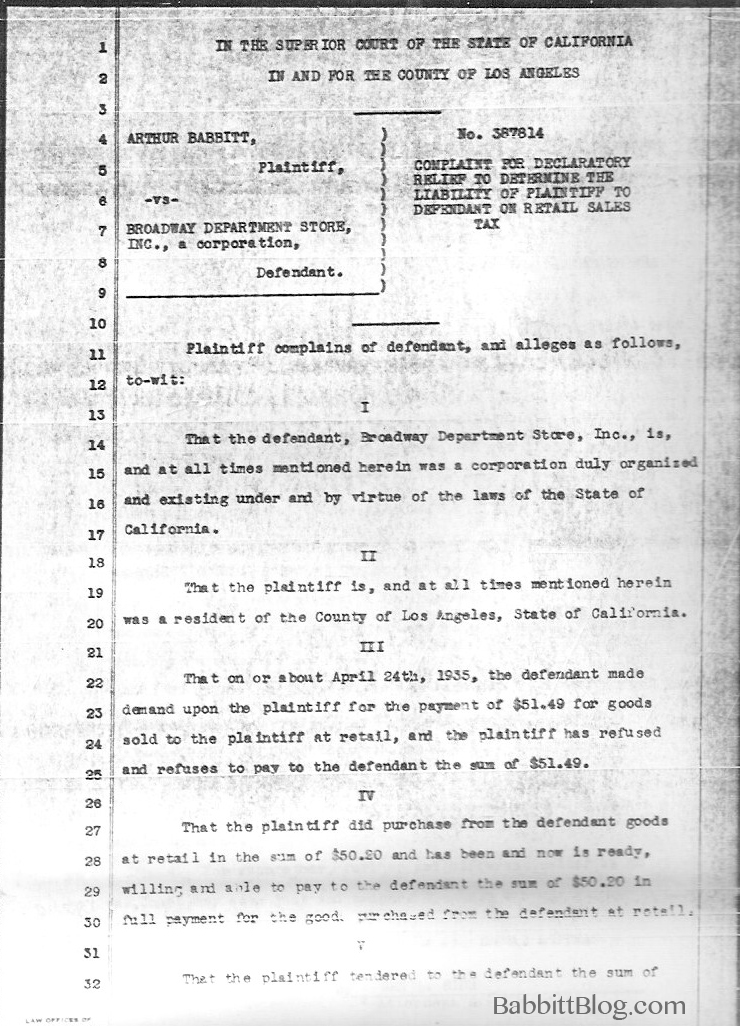

Disney animators would remember it for years to come as the occasion in which Babbitt sued a local merchant for a handful of pennies. It was studio gossip, and helped build Babbitt’s reputation as principled thorn-in-the-ass. It is likely that Babbitt, at 27, boasted to his colleagues of his assertion. On May 14 1935, he took the Broadway Department Store Inc. to court over sales tax.

To us, such an act seems ludicrous. But California sales tax was new to Babbitt. Well, newish.

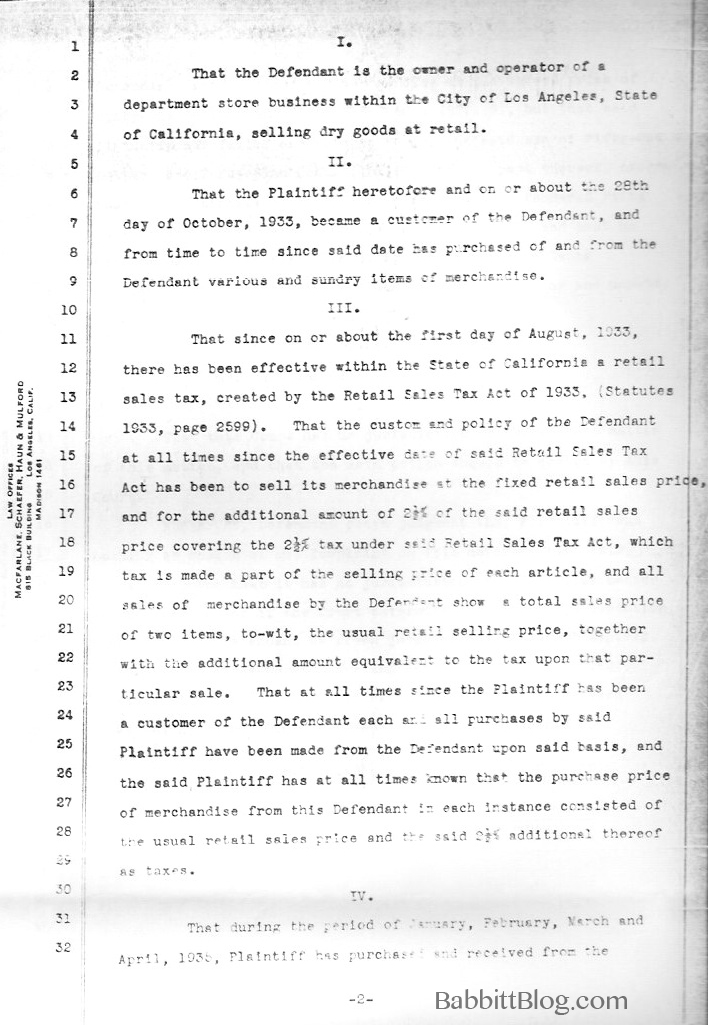

California state retail sales tax had just been established on August 1 1933, charging 2 ½ % on each purchase. Babbitt became a customer of the store that October. The store’s policy “at all times since the effective sate of said Retail Sales Tax Act has been to sell its merchandise at the fixed retail sales price, and for the additional amount of 2½% […]and all sales of merchandise by the Defendant show a total sales price of two items [ i.e .] the usual retail selling price, together with the additional amount equivalent to the tax upon that particular sale.”

What’s more, “The plaintiff has at all times known that the purchase price of merchandise from this Defendant in each instance consisted of the usual retail sales price and the said 2 ½ % additional thereof as taxes.”

Then, at the start of 1935, Babbitt decided he had a point to prove. From January through April, he was not going to pay his sales tax, and thus had not made a single payment on $51.49 worth of purchases he accrued. Around April 24th, the merchant demanded his money owed, and Babbitt refused to pay him the entire sum. He offered a check for the purchases minus the sales tax, totaling $50.20, and the merchant refused to accept it. Legally speaking, it was a controversy over who was liable over the $1.29 sales tax.

The merchant’s attorneys requested that “this Court determine that it has no jurisdiction of the subject matter of this action” and that the case be thrown out.

You have to wonder at the kind of lawyer that would take Babbitt’s case. I can only speculate what Ben L. Blue & Thomas Lippman, Babbitt’s attorneys, charged him for their services before and during the July 3 trial.

On November 18 the case was dismissed. As Klosterman writes,

“If every person who felt wronged pursed a lawsuit on principle, the court system would collapse (thereby delaying and complicating the cases of people in far more desperate situations than your own).”

Babbitt would encounter a more desperate situation in December 1941, when he brought a civil suit to Walt Disney.

Selected pages of Babbitt’s 1935 court case are shown below.